|

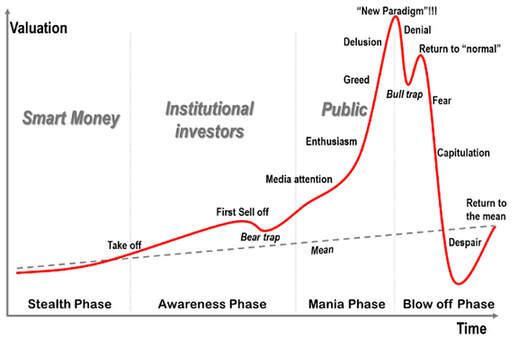

While it is certainly eye-catching, the title of this post falls into the same category as “How to go from Dad Bod to 6-Pack Abs in 2 Weeks.” Unfortunately, there is no quick and easy route to financial success. As you have probably heard, the stories of sudden windfalls of cash through the lottery, inheritance, or professional football signing bonuses typically don’t end well. This phenomenon can be partially explained by behavioral finance (the ways people think about and relate to money). Despite the name, this post will highlight a few financially healthy behaviors with proven long-term results. Have a plan in place You will need two plans—one that outlines the steps to your goals and one that outlines your backup plan or in-case-of-emergency plan. The first plan dictates what you would like to happen. For example, if you are going on a vacation, you will make a plan for your trip including flights, hotels, activities, etc. This will ensure you have a smooth, successful trip. Since life is unpredictable, an emergency plan is just as important as a primary plan. For example, your workplace probably has an emergency plan in case of a fire in the office (If you aren’t sure what to do in a fire, please see Dwight Schrute for best practices). You need both types of planning in your financial life. Whether you are aiming to get out of debt, pay for your kids’ college, buy a home, start a business, or travel more, you need to know the steps required to get there. If you attempt to make a financial plan on your own, Microsoft Excel will be your best friend. I would suggest separating your money into different accounts or “buckets” based on different goals. For example, keeping your kids’ college fund in a separate account than your vacation fund will (1) help you not dip into the savings for different goals and (2) help you track your progress toward your goals and ensure that you are not over-funding or under-funding a goal. Calculate how much you will need for your goal in how many years, and back into how much you will need to save for it. Overachievers can factor in investment growth and inflation for your goals, or most financial planners have software that can help you with this. Your emergency plan will carry you through the unexpected that will inevitably come at some point in your financial life. This may include medical bills, loss of income, inflation, unexpected loss, stock market corrections, and recessions. You will encounter these situations, but having a plan in place for what-if, scenarios will ease your mind. Your emergency plan dictates your next steps in stressful situations and will help you use your money effectively. Follow Dwight’s approach and simulate an emergency. Run through plausible scenarios on paper or in Excel and experiment with different responses. Your rehearsed response will pay dividends when the unexpected comes and you are prepared. Invest for the Long Haul When I started college, I thought investing was cool because you could make fast money without much work. I believed that investing for retirement was boring because it was so far away and didn’t sound like a fun goal. My attitude toward investing was short-term and focused on instant gratification. It didn’t take long to realize that investing is anything but easy and fast. Over the course of a year, my $2,000 investment grew to a measly $2,120. Woohoo! A year of locking up my money and all I had to show for it was enough money for two tanks of gas. The beautiful side of investing, however, is in the magic of compounding. My $2000 investment sounds a whole lot better considering that an investment of $2000 every year with a 6% compounded annual return would amount to $400,000 forty-five years later. $2,000 per year results in a four-fold growth by the age of retirement. When it comes to investing, start early and invest for the long haul. The longer you have your money invested, the more exponentially it will grow. That’s the magic of compound growth. In other words, if your investment earns $1000 this year, don’t use those earnings for short-term expenses such as a vacation or car. Instead, leave that money and let it grow. You won’t regret it. Live Below your Means This “super-fun” tip is important, but you will not reap its benefits right away. I don’t like the phrase “Live below your means” because it suggests that you have to option to live at a higher income level. It should not be an option to spend every penny you make. Savings is important. I prefer the phrase, “Pay yourself first.” Pay yourself first means that the first “bill” you pay with your paycheck is savings. Set a savings amount based on your goals. Everyone needs to save a different amount, but a good goal to work toward is 20% of your income. Having “savings” in your checking account to serve as a buffer when the unexpected comes is a good plan, but I would argue that you really need “savings” in your BUDGET to work as a buffer. Excess income covers a multitude of sins. Having this type of buffer brings a little more peace to your financial life. If you have this buffer, then you may not need to dig into your emergency fund to meet a financial need. Instead, you can use your excess income. This allows you to maintain a smaller emergency fund, and invest more of your money, thus earning more money. These are just a few reasons I would argue for building a buffer in your budget through savings. Understand Why You Do What You Do We are life-long learners, and personal finance is something that will always be a part of your life. Find someone who can help you learn – a parent, a mentor, or your financial planner/advisor. Notice that I don’t list “friend” here. Find someone who has a lot more experience than you in this area and can teach you from an expert perspective. Similar to my last blog post on taking financial advice from others, I would suggest double checking what you hear from others and coming to your own, educated conclusion. Writing out your financial beliefs and goals is a healthy practice that may encourage “staying the course” rather than following a “herd mentality.” Here’s an example of basic beliefs to guide investing: 1) Invest for the long-haul (2) Don’t try to time the market, and (3) Be skeptical of investments that promise sky-high returns.” Looking at these beliefs before you make an investment decision may protect you from following the crowd and investing in things that falsely promise miracle returns. The chart below by Jean-Paul Rodrigue (2017) shows the effects of the herd-mentality and how it creates investment bubbles.  Like this blog post? Check out these pages...

Comments are closed.

|

|

1701 W Northwest Hwy Ste 100

Grapevine, TX 76051 640 Taylor Street Ste 1200 Fort Worth, TX 76102 (817)-799-7699 |

|

© 2023 Flourish Financial Planning, Inc.. All rights reserved.